Why Your Spending Habits Matter More Than Your Income When Buying a Home

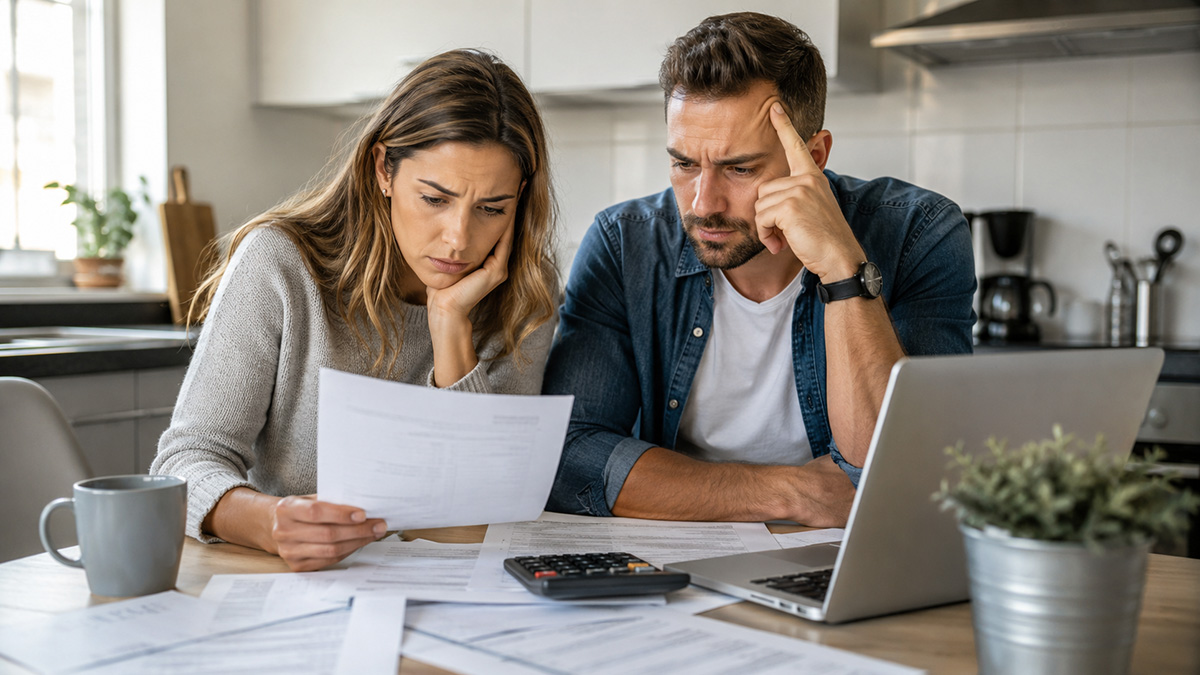

Many people believe that earning a higher income automatically makes buying a home easier. While income certainly plays an important role, it is only part of the equation. How you manage the money you earn can have an even greater impact on your ability to qualify for a mortgage and comfortably afford homeownership. Developing healthy spending habits before you begin your home search can put you in a much stronger financial position.

Many people believe that earning a higher income automatically makes buying a home easier. While income certainly plays an important role, it is only part of the equation. How you manage the money you earn can have an even greater impact on your ability to qualify for a mortgage and comfortably afford homeownership. Developing healthy spending habits before you begin your home search can put you in a much stronger financial position.

Create a Realistic Monthly Budget

Understanding where your money goes each month is one of the best ways to prepare for homeownership. Review your monthly income and expenses, including subscriptions, dining out, entertainment, and discretionary spending. Identifying areas where you can reduce unnecessary expenses may help you save more for your down payment, closing costs, and future home expenses.

Keep Your Debt Under Control

Mortgage lenders consider your debt-to-income ratio when evaluating your loan application. Even if you have a strong income, carrying large credit card balances or other monthly debt payments can affect how much home you can comfortably afford. Paying down debt before purchasing a home may improve your financial profile and provide greater flexibility in your monthly budget.

Build Healthy Financial Habits

Small financial decisions made consistently over time often have a greater impact than occasional large savings. Setting aside money each month, paying bills on time, and avoiding unnecessary purchases can strengthen your financial foundation. These habits not only prepare you for buying a home but also make it easier to manage the ongoing responsibilities of homeownership.

Think Beyond the Mortgage Payment

Owning a home involves more than making a monthly mortgage payment. Utilities, homeowners insurance, maintenance, and unexpected repairs should all be part of your financial plan. Buyers who develop strong budgeting habits before purchasing a home are often better prepared to handle these additional expenses without feeling overwhelmed.

Work With Your Mortgage Professional

A mortgage professional can help you understand how your overall financial picture affects your home buying options. Together, you can review your budget, discuss ways to strengthen your financial position, and determine a comfortable price range that supports your long-term goals.

Buying a home is not simply about how much money you earn. It is about how well you manage your finances before and after closing. By developing smart spending habits today, you can build the confidence and stability needed to enjoy homeownership for years to come.

Buying a home before your lease expires may seem like paying for two places at once, but in many cases it can actually make the transition smoother and less stressful. Every situation is different, and understanding your options can help you decide whether overlapping your lease and mortgage is the right move.

Buying a home before your lease expires may seem like paying for two places at once, but in many cases it can actually make the transition smoother and less stressful. Every situation is different, and understanding your options can help you decide whether overlapping your lease and mortgage is the right move. As closing day approaches, many homebuyers assume the mortgage process is nearly complete. While that is often true, lenders may continue reviewing your financial information until the final approval is issued. Even small changes to your finances can create new questions, require additional documentation, and potentially delay your closing. Knowing what to avoid can help keep your home purchase on track.

As closing day approaches, many homebuyers assume the mortgage process is nearly complete. While that is often true, lenders may continue reviewing your financial information until the final approval is issued. Even small changes to your finances can create new questions, require additional documentation, and potentially delay your closing. Knowing what to avoid can help keep your home purchase on track.