Why Small Financial Changes Can Delay Your Closing

As closing day approaches, many homebuyers assume the mortgage process is nearly complete. While that is often true, lenders may continue reviewing your financial information until the final approval is issued. Even small changes to your finances can create new questions, require additional documentation, and potentially delay your closing. Knowing what to avoid can help keep your home purchase on track.

As closing day approaches, many homebuyers assume the mortgage process is nearly complete. While that is often true, lenders may continue reviewing your financial information until the final approval is issued. Even small changes to your finances can create new questions, require additional documentation, and potentially delay your closing. Knowing what to avoid can help keep your home purchase on track.

New Credit Can Create New Questions

Opening a new credit card, financing furniture, or applying for a store account may seem harmless, but new credit can affect your mortgage file. Lenders may need to review the new account, calculate the monthly payment, and determine whether it changes your debt-to-income ratio. Waiting until after closing is usually the safer choice.

Large Deposits May Need Documentation

If a large deposit appears in your bank account, your lender may ask where the money came from. This is not unusual, but it can slow the process if records are not available. Funds from gifts, bonuses, transfers, or account withdrawals may need a clear paper trail before they can be accepted.

Changing Jobs Can Affect Timing

Even if a new job is a positive career move, changing employment before closing can require additional review. Lenders may need to verify your new position, confirm income details, and request updated documentation. If you are considering an employment change, speak with your mortgage professional first.

Moving Money Between Accounts Can Add Steps

Transferring funds between accounts may seem simple, but it can create additional documentation requirements. Lenders need to verify the source and movement of funds used for closing. Keeping your accounts consistent can make it easier to confirm available assets.

Small Choices Can Have Big Timing Impacts

Most financial changes do not automatically stop a mortgage approval, but they can add time to the review process. When closing deadlines are approaching, even a small delay can create stress for buyers, sellers, agents, and everyone involved in the transaction.

The safest approach is to keep your financial picture steady until after closing. Before opening credit, making large purchases, changing jobs, or moving money, contact your mortgage professional. A quick conversation can help you avoid preventable delays and get to closing day with greater confidence.

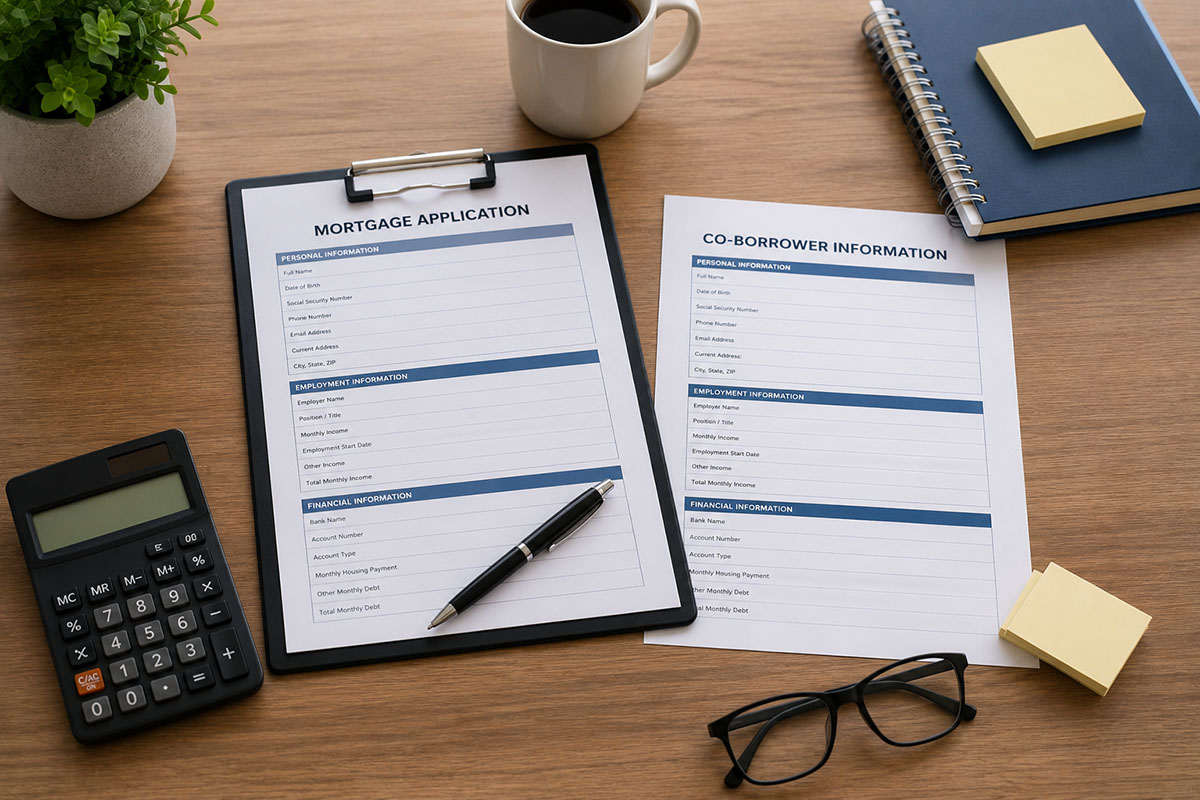

Buying a home is an exciting milestone, but qualifying for a mortgage may feel challenging for some buyers. If your income, credit profile, or purchasing power falls short of your homeownership goals, applying with a co-borrower may help strengthen your mortgage application. While adding another borrower is not the right solution for everyone, understanding how it works can help you make an informed decision.

Buying a home is an exciting milestone, but qualifying for a mortgage may feel challenging for some buyers. If your income, credit profile, or purchasing power falls short of your homeownership goals, applying with a co-borrower may help strengthen your mortgage application. While adding another borrower is not the right solution for everyone, understanding how it works can help you make an informed decision. The final month before closing is one of the most exciting parts of the home buying journey. It is also one of the most important times to keep your finances as stable as possible. Many buyers believe that once they receive loan approval, they can return to their normal spending habits. In reality, lenders often continue reviewing financial information until just before closing. Taking a few simple steps during these final weeks can help keep your mortgage on track and prevent unnecessary delays.

The final month before closing is one of the most exciting parts of the home buying journey. It is also one of the most important times to keep your finances as stable as possible. Many buyers believe that once they receive loan approval, they can return to their normal spending habits. In reality, lenders often continue reviewing financial information until just before closing. Taking a few simple steps during these final weeks can help keep your mortgage on track and prevent unnecessary delays.